In 2020, the COVID-19 pandemic struck, the S&P 500 index suffered the fastest 30% sell-off in its history, and the world went into a fury of chaos and lockdowns. In the midst of such calamity, I set out to do a review on my personal wealth and began to crystalize a financial plan moving forward.

I examined my overall financial portfolio from 2 aspects:

1) Portfolio Allocation

2) Cash Flow

8 Categories of Portfolio Allocation

1) Ready Cash Fund

– target at 3 months of expense budget

– need to replenish regularly

– no hurdle rate to cross

– main consideration is high liquidity

– main vehicles are bank accounts

2) Emergency Fund

– target at 1 year of expense budget

– set and forget unless needed for emergency

– set 2% p.a. hurdle rate to account for inflation

– also prefer high liquidity

– combination of insurance savings plans, fixed income investments

3) Healthcare Fund

– target at prevailing Basic Healthcare Sum (BHS) in MediSave Account (MA)

– interest rate at 4% p.a.

– complement with Integrated Shield Plan (ISP) and MediShield Life / ElderShield / CareShield Life (MSL/ES/CSL)

4) Insurance Fund

– Surrender Value (SV) of insurance policy

– set 3% p.a. hurdle rate

– combination of whole life and endowment plans

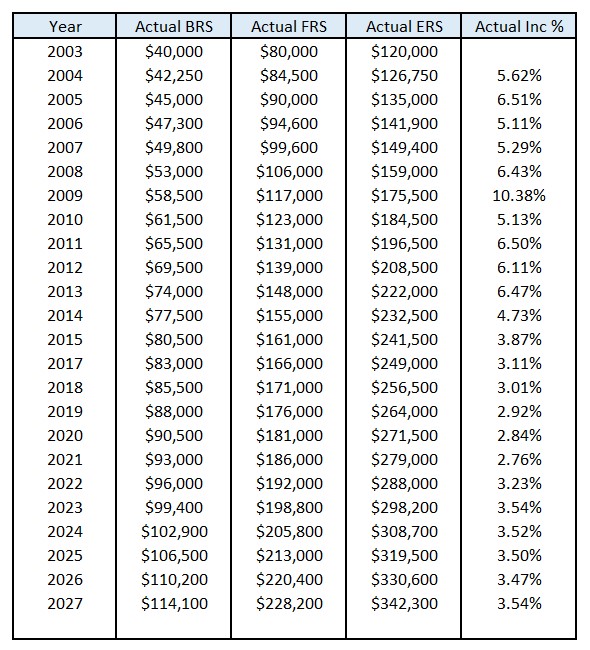

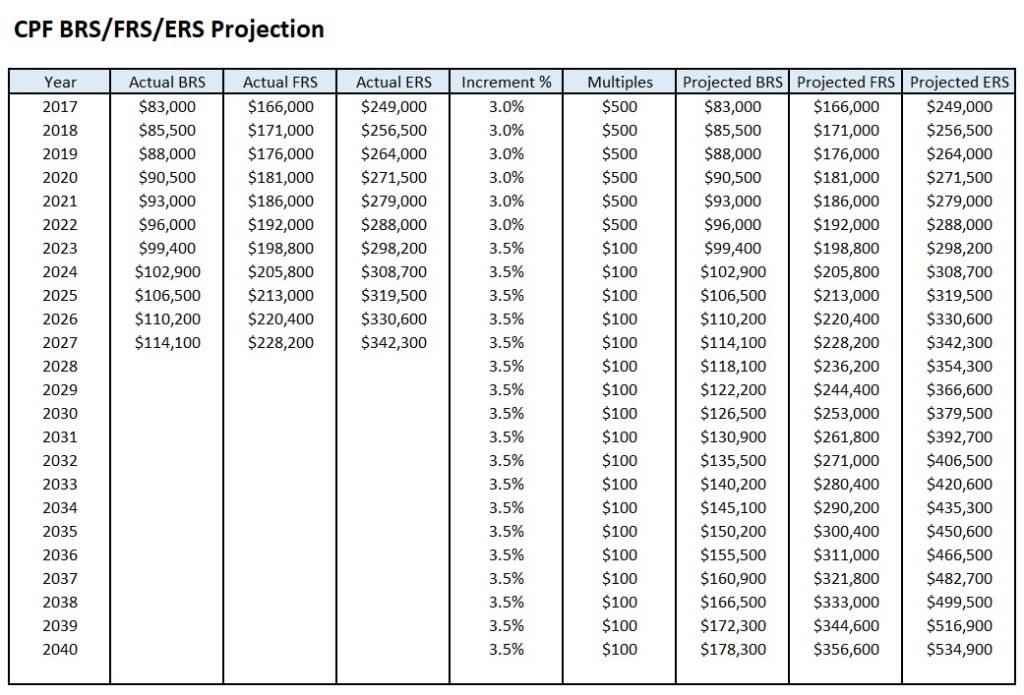

5) Retirement Fund

– target at prevailing Full Retirement Sum (FRS) in Retirement Account (RA)

– interest rate at 4% p.a.

– combination of Special/Ordinary Account (SA/OA) withdrawals and CPF LIFE payouts

6) Property Fund

– target at 30% of combined Property/Investment/Trading Fund

– set 4% p.a. hurdle rate

– aim for both capital gain and cash flow (rentals)

7) Investment Fund

– target at 60% of combined Property/Investment/Trading Fund

– set 6% p.a. hurdle rate

– aim for both capital gain and cash flow (dividends)

8) Trading Fund

– target at 10% of combined Property/Investment/Trading Fund

– no hurdle rate to cross, but aim for 12% p.a.

– speculative play, aim for cash flow, but prepare to lose all

2 Categories of Cash Flow

1) Pay Cheque

– intended for needs

– e.g. daily expenses, insurance premiums, loans, tax, bills, transport, medical, etc.

2) Play Cheque

– intended for wants

– e.g. tithes, travels, indulgence, investment, trading, charity, etc.

3-Bucket System

The above 8 categories of Portfolio Allocation are grouped under 3 buckets of funds:

1) Expense Bucket (3-Month Rolling Expenses, Replenish Regularly)

– Ready Cash Fund

2) Emergency Bucket (12-Month Expenses plus Medical & Legacy Needs)

– Emergency Fund

– Healthcare Fund

– Insurance Fund

3) Investment Bucket (Income & Growth, Feed Expense Bucket)

– Retirement Fund

– Property Fund

– Investment Fund

– Trading Fund

Personal Notes

1) Insurance Fund

– main consideration for insurance should be based on protection/legacy needs, rather than Return On Investment (ROI)

– need healthcare/hospitalization insurance to cater for growing medical expenses

– diminishing life insurance needs once we achieve self-insurance with wealth

– Surrender Value (SV) can be considered potential capital for Emergency Bucket and/or Investment Bucket

– monitor ROI of Annual Surrender Value Increment over Annual Premium Paid for consideration of whether and when to surrender the policy

2) Property for Own Stay

– property for own stay is not considered as an asset/investment, but rather a liability (mortgage loan, renovation, maintenance, property tax, etc.) from a cash flow perspective, unless we rent out some rooms with rent covering monthly expenses

– the property’s Mark-to-Market (MTM) value can only be realized on sales, and has to deduct the outstanding mortgage settlement, property agent fees, stamp duty, etc.

– when we sell the property, we will need to buy another property to stay

– if we manage to sell at high valuation, we will probably end up buying the next property at high valuation as well, unless we manage to pick up undervalued property, or downgrade, or rent for the next stay

– main consideration for selecting our own residential property should be convenience, comfort and affordability, rather than ROI

– we can think of HDB flat as a 99-year rent for a roof over our head

– we can unlock tail-end lease value by Lease Buyback Scheme (LBS)

– there are certainly undervalued property in the market, but just like stock picking, we really need to understand property selection well to pick the right property at the right location with the right price to be profitable as an investment

3) Core Satellite Portfolio Investment (CSPI) Strategy

– Core Portfolio investment are strategic, static, global, diversified and long term

– Satellite Portfolio investment are tactical, thematic, geographical, sectoral and mid term

– as a contrast to CSPI, trading are typically speculative, trend following, statistical, risk managed and short term